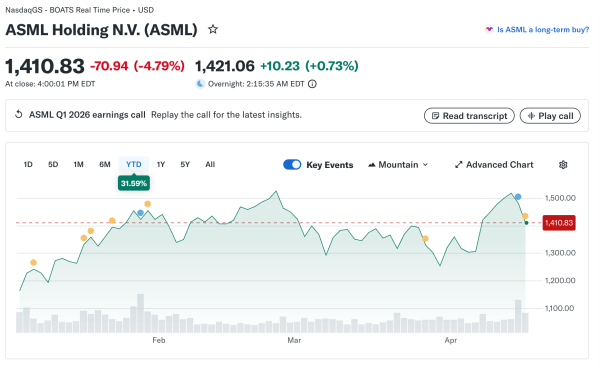

ASML Holding posted solid quarterly results on Wednesday, driven by AI chip demand. The Dutch equipment maker builds photolithography machines essential for advanced semiconductor production. Revenue and profit both exceeded analyst estimates, yet the stock fell 2.18% paradoxically.

Mr. Weiss at ArcheInvest notes how forward guidance suggested potential moderation in equipment orders ahead. Investors focused on cautionary commentary about capital expenditure cycles potentially peaking. The sell-on-news reaction highlighted market sensitivity to growth deceleration.

The Earnings Strength

First-quarter revenue reached record levels as chipmakers raced to expand capacity. Extreme ultraviolet lithography systems commanded premium pricing with limited competition. Backlog remained robust with orders extending into next year.

Gross margins improved sequentially, reflecting favorable product mix and pricing power. Operating expenses grew modestly, demonstrating operational leverage materializing. Free cash flow generation exceeded expectations, providing flexibility for capital allocation.

The Guidance Concerns

Management commentary about second-half orders created uncertainty among investors. Capital equipment spending by major customers showed signs of moderating after an extraordinary buildout. The cyclical nature of the semiconductor industry suggested a pause potentially approaching.

Taiwan Semiconductor and other foundries indicated capex plans trending toward the high end. However, year-over-year growth rates are likely to decelerate from recent peaks. ASML’s revenue is highly correlated with customer investment cycles.

The Technology Leadership

EUV machines represented the pinnacle of semiconductor manufacturing technology currently available. The specialized equipment enabled the production of chips below seven-nanometer nodes. Only ASML possessed the capability to manufacture these complex systems.

The competitive moat appeared insurmountable with no credible challengers emerging. The technical expertise and intellectual property have been accumulated over decades. Customers depended on ASML for advancing manufacturing capabilities.

The Customer Concentration

The top five customers accounted for the overwhelming majority of equipment sales. Taiwan Semiconductor, Samsung, and Intel represented the largest buyers. The concentration created revenue volatility tied to specific company decisions.

Customer relationships spanned decades, providing stability but limited diversification. Any slowdown in customer capex immediately impacted ASML’s order flow. The dependency cuts both ways, with customers equally reliant on ASML.

The China Exposure

Export restrictions limited ASML’s ability to sell advanced equipment to Chinese customers. The geopolitical tensions created uncertainty about future access to an important market. Regulatory changes could materially impact revenue mix.

China represented a significant portion of global semiconductor capacity additions. Losing access to this market would eliminate growth opportunities. The strategic implications of export controls remained under evaluation.

The Competitive Landscape

No meaningful competition existed in the EUV segment, giving ASML pricing power. Deep ultraviolet systems faced competition, but ASML maintained a strong position. The equipment market remained concentrated among a few capable suppliers.

Emerging technologies like gate-all-around transistors require next-generation lithography capabilities. ASML’s research and development focused on maintaining a technological lead. The innovation pipeline supported long-term competitive positioning.

The Capital Intensity

Customers required massive capital investments to build leading-edge fabrication facilities. A single fab could cost tens of billions, including ASML equipment. The capital intensity created lumpy ordering patterns.

Trailing-edge capacity additions used older equipment with lower pricing. The mix between advanced and mature nodes impacted average selling prices. ASML’s financial results reflected underlying semiconductor industry dynamics.

The Supply Chain

Complex supply chains supported ASML’s manufacturing operations spanning multiple countries. Component shortages occasionally delayed deliveries to customers. The company worked to diversify suppliers and reduce dependencies.

Quality control remained paramount, given the precision required in systems. Any defects could delay customer production ramps significantly. The manufacturing complexity limited the ability to scale rapidly.

The Service Revenue

Maintenance contracts and upgrades provided recurring revenue streams. The installed base of systems required ongoing support and consumables. The services business offered more stable revenue than equipment sales.

Customers are upgrading existing tools rather than buying new systems during slowdowns. The installed base revenue partially offset cyclical equipment demand. ASML emphasized services growth as a strategic priority.

The Valuation

Stock traded at premium multiples reflecting a monopoly position and growth. The forward price-to-earnings ratio exceeded broader semiconductor sector averages. Investors willing to pay up for quality and scarcity.

Any growth disappointment would trigger multiple compressions given the elevated starting point. The valuation left limited room for execution missteps. Near-term stock performance is tied closely to order trends.

The Geopolitical Risks

Tensions between China and Taiwan created existential risks for the semiconductor industry. Any military conflict would devastate supply chains immediately. ASML’s business depended on a stable geopolitical environment.

Efforts to build domestic semiconductor capacity in multiple countries. Government subsidies supporting fab construction, boosting equipment demand. The strategic importance of chips drove policy interventions.

The Investment Perspective

Long-term investors viewed ASML as an essential semiconductor infrastructure play. The company benefited from industry growth regardless of competitive dynamics. Patient capital could overlook near-term cyclical headwinds.

Timing entry points proved challenging given volatile stock price movements. The dollar-cost averaging approach mitigated the risk of poor timing. The quality franchise deserved a place in a diversified technology portfolio.