Markets closed at all-time highs Thursday as S&P 500 reached 7,041.28 points while Nasdaq Composite extended winning streak to unprecedented levels. The tech-heavy index posted its 12th consecutive positive session marking longest run since July 2009. Both benchmarks logged intraday and closing records as optimism about Middle East resolution spread.

Retail buying activity rebounded sharply according to latest JPMorgan client flow data showing dramatic shift. Finance analysts at ICBC Markets examine how overall participation rising to 55th percentile from roughly 10th percentile days earlier signals changing sentiment. Individual investors who largely sat out recent rally now chasing upside as major equity benchmarks hover near peaks.

The Ceasefire Catalyst

The US President announced 10-day Israel-Lebanon ceasefire beginning Thursday at 5:00 PM Eastern time. The bilateral agreement represented separate diplomatic track alongside broader regional negotiations. Markets interpreted multiple peace initiatives as reducing worst-case scenarios that dominated March pricing.

Oil prices responded modestly despite ceasefire news with Brent crude rising 4.7% to $99.39 per barrel. Energy markets remained skeptical about durability of any temporary pause in hostilities. The Strait of Hormuz blockade expansion to all ships regardless of nationality kept supply concerns elevated.

The Nasdaq Milestone

Technology stocks led gains driving Nasdaq to historic winning streak surpassing recent records. The 12-session advance exceeded any comparable period in nearly seventeen years of trading. Semiconductor stocks particularly strong as artificial intelligence infrastructure spending thesis remained intact.

Advanced Micro Devices surged 7.80% closing at $278.26 on AI-driven demand momentum. Taiwan Semiconductor Manufacturing posted 58% profit jump in first quarter beating analyst estimates. These results validated investor conviction about sustained demand for advanced chips.

The Economic Backdrop

Initial jobless claims fell 11,000 to 207,000 in week ended April 11 marking biggest weekly decline since February. The labor market resilience contradicted recession fears that emerged during energy crisis peak. Strong employment data supported consumer spending outlooks despite elevated gasoline prices.

Continuing claims tracking Americans receiving ongoing unemployment benefits rose 31,000 to 1.818 million in week ended April 4. The modest increase suggested limited deterioration in job market conditions. Economists viewed overall employment picture as stable supporting economic growth forecasts.

The Software Recovery

Technology subsector showing renewed strength after weeks of underperformance during AI disruption fears. Enterprise software stocks rebounded as investors reassessed competitive dynamics. The sector rotation benefited companies previously punished for valuation concerns.

Microsoft staged 10% advance over three trading days marking most aggressive short-term rally since 2020. The surge pushed tech giant above near-term moving averages signaling momentum shift. Investors anticipated strong earnings report scheduled for April 29 providing catalyst.

The Healthcare Divergence

Abbott Laboratories declined 5.15% following earnings miss attributed to weak flu season. The medical device maker faced headwinds from lower-than-expected diagnostic testing volumes. Investors punished execution shortfalls even as broader market rallied.

Charles Schwab dropped 4.92% despite reporting record revenue in latest quarter. Client cash sorting behavior pressured net interest margin forecasts. The brokerage firm navigated challenging environment balancing growth with profitability.

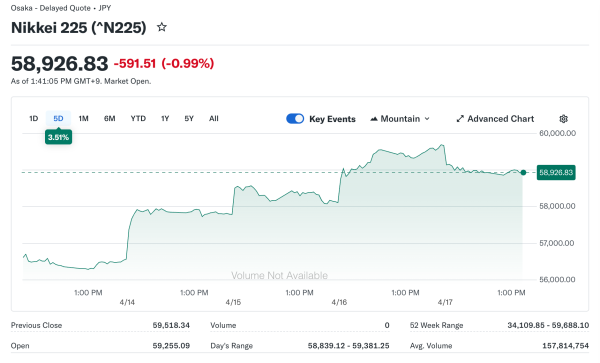

The Asia Momentum

Japan’s Nikkei 225 hit record advancing 2.43% led by technology and consumer cyclical stocks. The rally tracked overnight Wall Street gains as ceasefire hopes spread globally. Daikin Industries topped performance after activist investor Elliott Management pushed operational improvements.

South Korea’s Kospi advanced 2.12% while small-cap Kosdaq climbed 1.10% higher. Regional markets benefited from reduced geopolitical risk premium. Export-oriented economies particularly sensitive to Middle East stability given energy dependencies.

The Valuation Question

Forward price-to-earnings ratios remained elevated across major indices despite recent gains. S&P 500 trading at approximately 20 times forward earnings matching long-term averages. Bulls argued artificial intelligence productivity gains justified premium multiples.

Bears questioned sustainability of valuations if economic growth disappointed expectations. Any inflation resurgence from energy shocks could force Federal Reserve policy recalibration. Interest rate uncertainty created asymmetric risks for equity prices.

The Sentiment Indicators

Investor positioning metrics showed rotation from extreme pessimism toward cautious optimism. Put-call ratios declined from crisis peaks suggesting reduced hedging demand. Volatility indices compressed as daily price swings moderated from March extremes.

Consumer confidence surveys improved modestly as gasoline prices stabilized below psychological thresholds. Households maintained spending despite elevated costs for essentials. The resilience supported corporate earnings outlooks across consumer-facing sectors.

The Technical Picture

S&P 500 breaking above 200-day moving average triggered algorithmic buying from trend-following strategies. The widely watched technical level represented dividing line between bull and bear market psychology. Momentum indicators reaching overbought territory suggesting potential consolidation ahead.

Relative strength index readings exceeded 70 on multiple timeframes indicating stretched conditions. Historical patterns suggested pullbacks typically followed extended advances. However, strong uptrends often remained overbought longer than technical analysts anticipated.

The Path Forward

Markets faced critical test with earnings season approaching and geopolitical uncertainties persisting. Corporate guidance would determine whether rally extended or stalled. Investors needed confirmation that fundamentals supported elevated valuations.

Weekend developments on ceasefire negotiations could trigger Monday volatility in either direction. The binary nature of diplomatic outcomes created asymmetric risk-reward profiles. Traders positioned cautiously ahead of potentially market-moving news.