Warren Buffett is famous for spotting long-term winners before the market fully appreciates them, and his latest move shows that sometimes, the most unassuming businesses can be the most rewarding.

In a recent analysis by Tarillium, the firm highlighted how Buffett’s quiet accumulation of Pool Corp. (NASDAQ: POOL), the world’s leading distributor of swimming pool supplies and maintenance products, reflects his signature strategy of buying durable, cash-generating companies long before they become market darlings.

Buffett’s Big Bet on a Quiet Compounder

According to Berkshire Hathaway’s filings, Buffett increased his stake in Pool by more than 750% since first purchasing shares last year, a striking vote of confidence in a business many investors overlook. Pool Corp’s dominance spans over 450 distribution centers across North America, Europe, and Australia, giving it an unmatched moat in the industry.

The company doesn’t just sell pool products; it powers an entire ecosystem of maintenance services, renovations, and essential upkeep. This steady demand creates resilience even when discretionary spending weakens, aligning perfectly with Buffett’s philosophy of owning enduring, cash-generating businesses.

A Durable Moat and Stable Cash Engine

What Buffett likely sees in Pool Corp is a fortress-like competitive advantage. Replicating its logistics, customer relationships, and product reach would require enormous capital and time, something rivals simply can’t match.

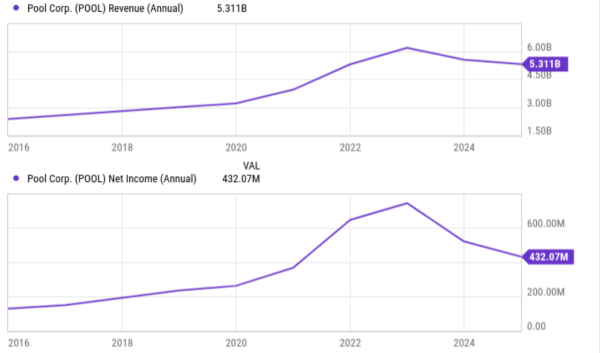

Despite a slowdown in pool construction due to higher interest rates, Pool’s maintenance segment provides recurring, high-margin revenue that smooths out earnings volatility. During 2024’s “tempered discretionary spending” environment, maintenance sales held steady and helped deliver $5.3 billion in annual revenue, proof of operational durability.

Consistent Growth and Resilience Through Cycles

Over the past decade, Pool has reported triple-digit growth in both revenue and net income, driving its share price up more than 200% in that same period. The company’s most recent quarter underscores that momentum:

- Sales: Up 1% year-over-year to $1.8 billion

- Earnings per share: Rose 4% to $5.17

- Gross margin: A solid 30%, reflecting disciplined pricing and cost control

This consistency appeals to Buffett’s love of “sleep-well-at-night” businesses, those that perform well in good times and hold steady when the economy softens.

The Macro Tailwind Ahead

Looking ahead, Pool could be poised for renewed acceleration. Lower interest rates would ease financing pressures for homeowners and builders, likely reviving discretionary pool projects. Combined with the company’s strong brand and distribution moat, that creates a favorable backdrop for earnings expansion in 2026 and beyond.

Analysts note that Pool’s hybrid model, balancing cyclical new builds with recurring maintenance, gives it a blend of growth and stability rare in today’s market. As macro pressures ease, those dual engines could drive outsized shareholder returns.

Valuation: A Buffett Bargain

For long-term investors, valuation always sits at the heart of Warren Buffett’s philosophy, and Pool Corp. (NASDAQ: POOL) currently checks that box. Shares trade at roughly 26× forward earnings, notably lower than the 35× multiple the stock commanded just a year ago, a significant compression that reflects short-term macro headwinds rather than any deterioration in the company’s fundamentals.

For a market leader with decades of pricing power, stable cash flow, and resilient recurring revenue from its maintenance segment, that kind of discount looks appealing. Pool’s business model is built on essential pool chemicals, equipment, and repair services, which generate steady demand even in slower construction cycles. This stability, combined with the company’s unmatched distribution network and supplier relationships, gives it a moat that competitors find hard to replicate.

In other words, Pool embodies the type of company Buffett loves: a high-quality operator with durable economics trading at a temporarily depressed valuation. As interest rates ease and discretionary spending rebounds, investors may soon reprice Pool upward, offering patient shareholders an opportunity to accumulate what many analysts describe as a “Buffett-style compounder hiding in plain sight.”

Final Takeaway

Tarillium’s investment desk views Pool Corp as a classic Buffett-style compounder a steady performer with dependable cash flows, a defensible market position, and long-term optionality tied to housing, outdoor living, and infrastructure upgrades.

In a market dominated by flashy AI names and speculative growth plays, Pool represents something rarer: a quiet, cash-rich business with compounding potential.

Buffett’s growing stake suggests confidence that slow and steady can still win big, and investors looking for sustainable wealth creation might want to take a page from his playbook before the market catches up.

Pool Corp may not grab headlines, but it embodies the timeless Buffett formula: a strong moat, consistent earnings, and patient growth. For those seeking stability with upside, this “boring” stock could end up making investors and Buffett a lot richer in the years ahead.